With threats of U.S. tariffs on Canadian goods and Canada’s decision to retaliate, the economic outlook for 2025 has become more uncertain. These trade tensions could hit BC’s economy, affecting jobs, prices, and even the housing market. But what do tariffs actually do, and how would this trade dispute impact real estate in British Columbia? Let’s break it down.

A tariff is a tax that one country places on imported goods from another country. The idea is to make foreign products more expensive, encouraging people to buy local instead.

Example: If the U.S. places a 25% tariff on Canadian lumber, an American company that used to pay $1,000 for Canadian wood will now have to pay $1,250. $1,000 to Canada for the wood and $250 to the American government to pay for the tariff. This might push them to buy from an American supplier instead, reducing demand for Canadian exports.

Since Canada and the U.S. are major trading partners, tariffs can have huge ripple effects on both economies—including job losses, rising prices, and a slowdown in real estate activity.

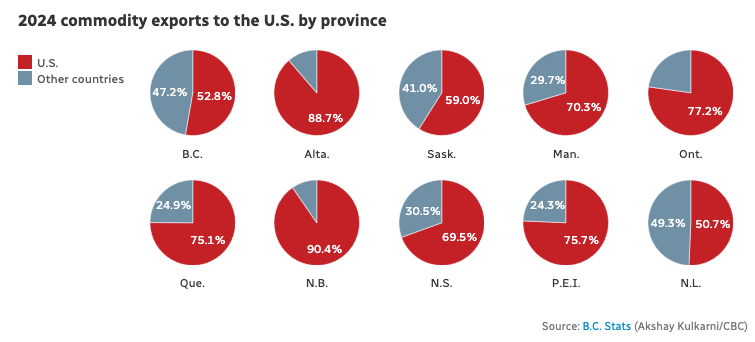

The good news for us is that BC is less dependent on U.S. trade than provinces like Alberta or Ontario, but 55% of BC’s exports still go to the U.S. Some of the hardest-hit industries will include:

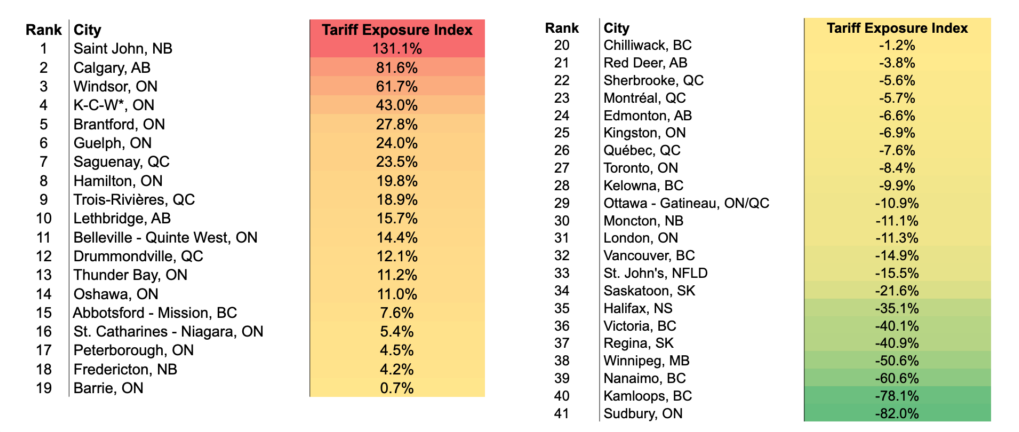

About 136,000 BC jobs are tied to exports to the U.S. If tariffs cause companies to cut jobs, fewer people will be able to afford homes, which could slow down real estate sales—especially in areas with high employment in affected industries. Areas, such as Greater Vancouver, whose economies are less dependent on the tariffed industries will be impacted less.

When Canada imposes tariffs on U.S. goods, the cost of those goods rises for Canadian consumers and businesses. If Canada places a 20% tariff on U.S. steel, for example, Canadian companies that use steel for construction will have to pay a 20% tax to the Canadian government to import the steel. These higher costs are usually passed down to consumers, leading to higher prices on products the steel is used for.

Higher tariffs = higher costs for businesses and consumers = higher inflation.

The Bank of Canada (BoC) has two main jobs:

If tariffs push inflation up (by increasing the price of goods), the BoC may raise interest rates to slow down price increases. However, if tariffs cause a recession (by slowing economic growth and job losses), the BoC may lower rates to stimulate the economy.

What happens next depends on how severe the impact is:

While the tariffs could present significant challenges to the economy and housing market, no outcome—positive or negative—is certain. At the time of this writing, the US announced they were, once again, delaying the tariffs until April, so the only thing that’s certain is that understanding these dynamics is crucial for stakeholders to navigate the evolving landscape effectively. If you're thinking about buying or selling, now is the time to stay informed and make a plan. Reach out, and let's talk about the best strategy for you in this evolving market.

What Is a Tariff? And How Do They Work?

A tariff is a tax that one country places on imported goods from another country. The idea is to make foreign products more expensive, encouraging people to buy local instead.

Example: If the U.S. places a 25% tariff on Canadian lumber, an American company that used to pay $1,000 for Canadian wood will now have to pay $1,250. $1,000 to Canada for the wood and $250 to the American government to pay for the tariff. This might push them to buy from an American supplier instead, reducing demand for Canadian exports.

Since Canada and the U.S. are major trading partners, tariffs can have huge ripple effects on both economies—including job losses, rising prices, and a slowdown in real estate activity.

BC Would Be Hit, But Not as Hard as Other Provinces

The good news for us is that BC is less dependent on U.S. trade than provinces like Alberta or Ontario, but 55% of BC’s exports still go to the U.S. Some of the hardest-hit industries will include:

- Energy (27% of BC’s exports to the U.S.) – Natural gas and electricity exports will be taxed, making them less competitive.

- Forestry (24% of BC’s exports to the U.S.) – The softwood lumber industry is already struggling, and new tariffs could lead to mill closures and job losses—just like what happened with past lumber disputes.

- Manufacturing – BC produces industrial machinery, aluminum, and construction materials, all of which are now subject to U.S. tariffs.

Job Losses Could Lead to Lower Housing Demand

About 136,000 BC jobs are tied to exports to the U.S. If tariffs cause companies to cut jobs, fewer people will be able to afford homes, which could slow down real estate sales—especially in areas with high employment in affected industries. Areas, such as Greater Vancouver, whose economies are less dependent on the tariffed industries will be impacted less.

How Canada’s Retaliation Tariffs Could Affect Inflation

When Canada imposes tariffs on U.S. goods, the cost of those goods rises for Canadian consumers and businesses. If Canada places a 20% tariff on U.S. steel, for example, Canadian companies that use steel for construction will have to pay a 20% tax to the Canadian government to import the steel. These higher costs are usually passed down to consumers, leading to higher prices on products the steel is used for.

Higher tariffs = higher costs for businesses and consumers = higher inflation.

How the Bank of Canada Responds to Inflation

The Bank of Canada (BoC) has two main jobs:

- 1. Keep inflation under control (targeting 2%)

- 2. Support economic growth

If tariffs push inflation up (by increasing the price of goods), the BoC may raise interest rates to slow down price increases. However, if tariffs cause a recession (by slowing economic growth and job losses), the BoC may lower rates to stimulate the economy.

What happens next depends on how severe the impact is:

- If inflation jumps too much, the BoC could raise interest rates to cool it down, making mortgages more expensive.

- If a recession hits, the BoC could lower interest rates, making borrowing cheaper and potentially boosting home sales.

- If a recession hits, the BoC could lower interest rates, making borrowing cheaper and potentially boosting home sales.

Mortgage rates could swing anywhere from 2.5% (if rates are cut) to 6.25% (if rates rise to fight inflation), depending on how the situation unfolds.

1) Higher Construction Costs = More Expensive Homes

Tariffs on U.S. building materials (like steel and lumber) will increase the cost of new home construction. This could mean higher prices for new homes and renovations in BC.

2) Economic Uncertainty Could Slow Home Sales

If BC’s economy slows due to job losses and lower exports, buyers may hold off on purchasing homes, leading to a temporary dip in real estate activity. As we have seen from previous recessions, the usual pattern for the BC housing market is an immediate decline in housing activity and then a strong recovery as the central bank lowers rates to stimulate the economy. However, the effect on inflation caused by Canadian retaliation and the Bank's ability to lower rates could short-circuit the normal pattern.

3) Mortgage Rates Are a Wildcard

If the economy slows down, lower interest rates could encourage more buyers—leading to a market rebound. But if inflation surges, higher mortgage rates could make buying a home even more expensive.

What Does This Mean for BC’s Real Estate Market?

1) Higher Construction Costs = More Expensive Homes

Tariffs on U.S. building materials (like steel and lumber) will increase the cost of new home construction. This could mean higher prices for new homes and renovations in BC.

2) Economic Uncertainty Could Slow Home Sales

If BC’s economy slows due to job losses and lower exports, buyers may hold off on purchasing homes, leading to a temporary dip in real estate activity. As we have seen from previous recessions, the usual pattern for the BC housing market is an immediate decline in housing activity and then a strong recovery as the central bank lowers rates to stimulate the economy. However, the effect on inflation caused by Canadian retaliation and the Bank's ability to lower rates could short-circuit the normal pattern.

3) Mortgage Rates Are a Wildcard

If the economy slows down, lower interest rates could encourage more buyers—leading to a market rebound. But if inflation surges, higher mortgage rates could make buying a home even more expensive.

Stay Informed

While the tariffs could present significant challenges to the economy and housing market, no outcome—positive or negative—is certain. At the time of this writing, the US announced they were, once again, delaying the tariffs until April, so the only thing that’s certain is that understanding these dynamics is crucial for stakeholders to navigate the evolving landscape effectively. If you're thinking about buying or selling, now is the time to stay informed and make a plan. Reach out, and let's talk about the best strategy for you in this evolving market.